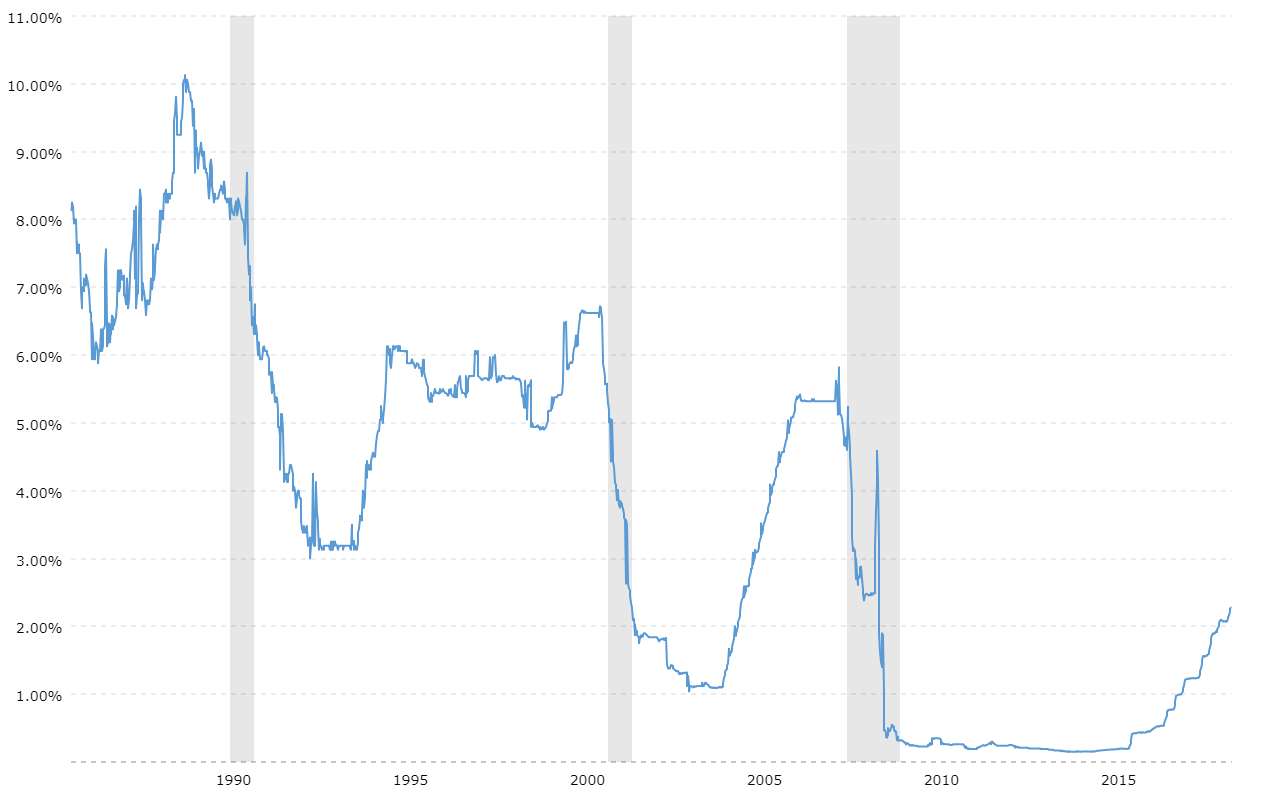

The Mortgage Bankers Organization's most current Weekly Application shows an uptick in applications for the week ending July 17, 2020. The Marketplace Compound Index enhanced by 4.1% from the previous week on a seasonally changed basis. Refinancing task showed continued eagerness, raising by 5.3% from the previous week, while purchasing task increased reasonably by 1.8%. The MBA's 30-year fixed-rate home loan rate inched up by one basis indicate 3.2% from the document low gotten to in the previous week.

Experts caution that this choice only prefers those that anticipate to stay in the residence for a short-term. Choosing an ARM over a fixed-rate home mortgage can be a strong financial choice, possibly conserving you countless bucks. You need to constantly ask your lending institution to describe ARM risks as well as precisely how much the settlements could increase.

- Accessibility to Electronic Services may be limited or unavailable during durations of peak need, market volatility, systems upgrade, maintenance, or for various other factors.

- Many individuals pick ARMs because they at least in the starting cost less interest than a fixed-rate mortgage.

- Interest-only lendings are really uncommon, and purchasers that want an ARM usually require greater credit rating and have to put more money down than customers who desire a fixed-rate home mortgage.

- Your lender picks which index to base your price on when you make an application for the finance, however the LIBOR is one of the most popular index utilized.

- When you're contrasting lending options, there are some special numbers to take note of when looking specifically at ARMs.

These caps run relative to just how typically their rate of interest modifications, how much it can increase from duration to period, in addition to an overall passion rise over the lifetime of the financing. Although it may seem like an intro price, your budget plan will certainly delight in the initial reduced regular monthly settlements. With that, you might have the ability to place more toward your primary every month. The margin applied to your ARM depends upon your credit history as well as credit history, in addition to a conventional margin that recognizes home loans are naturally riskier than the types of finances indexed by the benchmarks. The most creditworthy consumers will certainly pay near to the standard margin on home loans, and riskier loans will be additional increased from there. A fixed-rate home mortgage can use even more certainty due to the fact that it maintains the same rate of interest for the life of the funding.

Today's Prices

All web content is given on an "as is" basis, without any guarantees of any type of kind whatsoever. Details from this document may be used with appropriate attribution. Alteration of this document or its material is strictly banned. If you're wanting to get a home, you may be overwhelmed with the large number of mortgage selections.

Types Of Home Loan For Purchasers As Well As Refinancers

Maybe most important, Kaul believes, is the comparison in between the principles of both markets. A decade earlier, speculation and also greed increased costs, whereas now, in a supply-starved market, "demand" might be equally as easily identified as "requirement" for housing, of any type of kind. A 5/1 https://www.businessmodulehub.com/blog/4-things-to-know-before-buying-your-first-real-estate-property/ ARM offers an initial price for five years prior to resetting. Learn here Donna Fuscaldo is a self-employed journalist with 15+ years of experience as an economic reporter specializing in market news as well as political news. Donna is also a specialist in individual financing and spending topics.

Many individuals that bought homes with 7/1 or 5/1 ARMS in the decades before 2008 gained from the steady reduction in home mortgage prices during that time, as their ARM rates maintained resetting lower and also reduced. Many ARM home loans are "crossbreed" fundings with a set rate for the very first few years prior to the price starts adjusting, usually after 3, 5, 7 or ten years, after which the financing normally readjusts eery year afterwards. A 5-1 ARM is a financing where the rate is fixed for five years, after that resets every year after that; a 7-1 ARM is a fixed rate for the initial seven years and more. To truly get a feeling for an ARM, allow's do an example comparing it with a fixed-rate home mortgage for a $250,000 finance amount.

The words "variable" as well as "adjustable" are frequently used reciprocally. When individuals describe variable-rate home mortgages, they likely imply a home loan with a flexible rate. A real variable-rate home mortgage has an interest rate that transforms every month, however these aren't common. Nevertheless, for some home customers, especially those that move commonly or are getting starter homes, ARMs might make even more feeling. If you're denying your forever home, after that purchasing a house with an ARM and also selling it prior to the fixed-rate duration ends can mean a reduced home loan payment.

As an example, if you plan to sell the residence prior to the rate of interest starts to adjust, how to get rid of my timeshare legally those potential modifications may not be a trouble for your budget plan. For that reason, the price and repayment results you see from this calculator may not reflect your real situation. You might still qualify for a finance even in your circumstance does not match our presumptions.

That gets you the good old 2012 rates of interest, without offering every little thing you have on ebay.com to pay your discount factors. For a $300,000 home loan, getting from 4.2 percent to 3.33 percent can cost you $18,000 to $24,000. But just 2 that don't include the greater settlements of a 15-year mortgage. " It will certainly be time to stress if loan standards begin to unwind and anybody that can mist a mirror has the ability to obtain a mortgage. That is not what is happening now."

Along with differing car loan types as well as terms, you'll need to make a decision whether you desire a fixed-rate lending or a flexible rate mortgage. Flexible price home mortgages are occasionally marketed to consumers who are unlikely to pay off the car loan ought to rates of interest climb. In the USA, severe cases are characterized by the Customer Federation of America as predative loans. However along with various other customer supporters, she recognizes that reforms established given that the real estate crash have actually helped reduce the risks of adjustable-rate fundings by needing lending institutions to confirm a borrower's payment capacity. The most dangerous as well as aggressive adjustable-rate mortgages-- such as car loans with below-market "intro prices" that were made to increase dramatically, have additionally been eliminated.